Current Balance: $29,842.77

Once you’ve set your goal, i.e. targeted date, to pay off your school loans. how do you determine how much to pay off each week, month or year depending on your preference in payment? You create an amortization schedule in excel and have some fun.

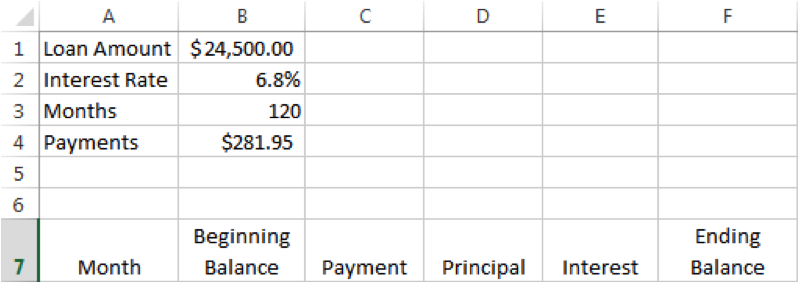

The first step is creating your based amortization schedule with either the default repayment schedule or your preferred repayment schedule. So let’s get started. For this example I’m going to calculate three difference loans with differing balances and interest rates with a standard repayment schedule of ten (10) years or 120 months.

Loan Amount Interest Rate

Loan 1 $24,500 6.8%

Loan 2 $12,200 3.5%

Loan 3 $ 5,000 5.0%

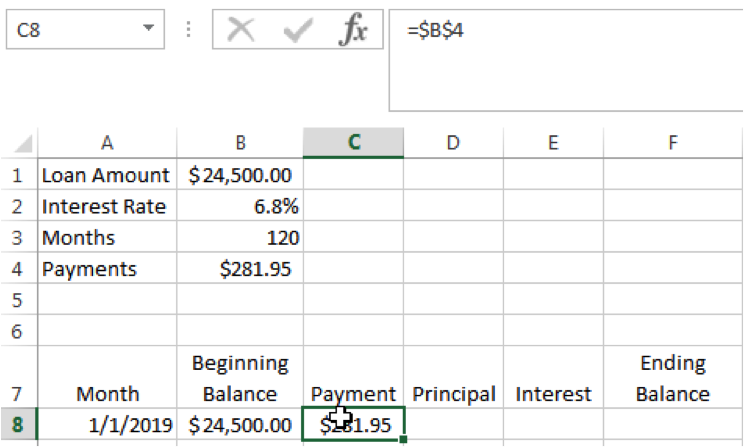

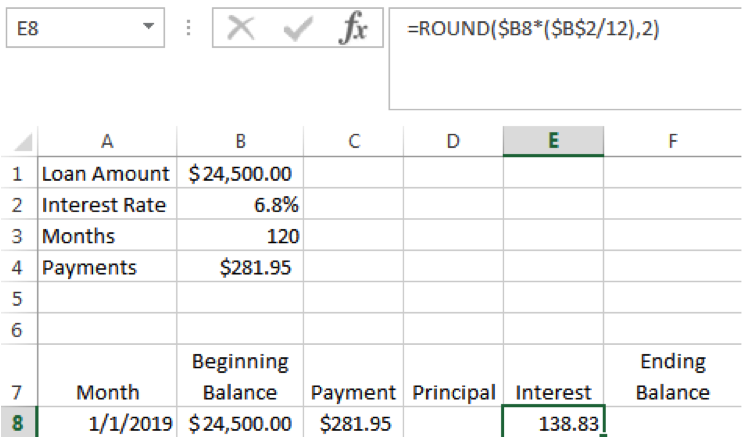

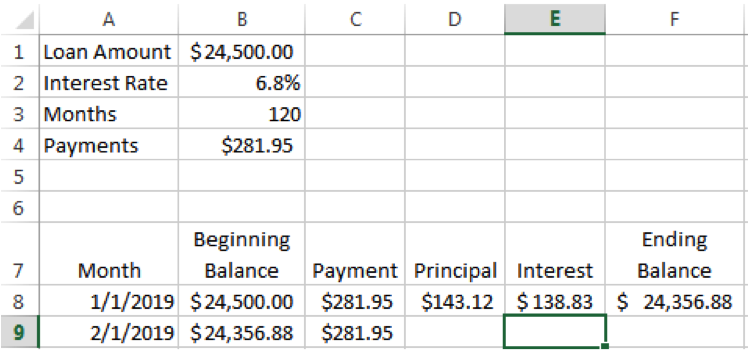

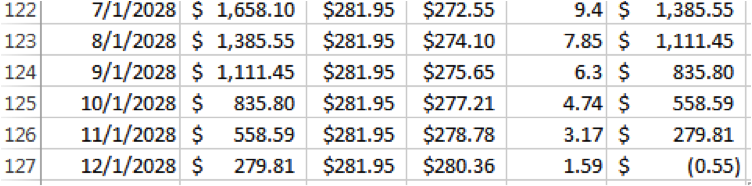

Insert your loan information into Excel which should look something like this: